If the adjustment will impact or change the data on your quarterly return, you might consider doing a quarter-to-date adjustment instead of a year-to-date adjustment. Most businesses must submit their last month’s payroll deductions to the Canada Revenue Agency (CRA) by the 15th of the current month. If the Installments-Payroll account has an amount remaining at year-end, confirm with your tax agency if the remaining amount will be carry-forward to the next year. If the Installments-Payroll account has a balance medical expenses retirees and others can deduct on their taxes owing (a negative amount), you may need to remit the balance to the tax agency.

Common scenarios that can be corrected by a liability adjustment

You can generate payroll liability reports or review the individual liability accounts to ensure that the adjustments align with your requirements. In this article, we will guide you through the steps to adjust payroll liabilities in QuickBooks Online, providing you with two options to choose from. Whether you prefer using the Payroll Center or the Chart of Accounts, both methods offer a straightforward approach to making adjustments. For instance, if an employee’s vacation pay is adjusted retroactively, it would prompt a change in the accrued vacation liability.

Pay or adjust payroll liabilities in QuickBooks Desktop

Now let’s move on to making changes to the payroll tax liabilities in QuickBooks, but before that ensure you have the latest payroll tax table updates installed. You’ll just need to enter the date, amount, and payroll liability items that are shown on the report. Remember, when adjusting payroll liabilities, it is crucial to exercise caution and attention to detail.

- This will enable you to maintain accurate financial records, comply with tax regulations, and make informed decisions based on reliable payroll data.

- This will help you keep track of your payroll details and history, especially at year ends.

- This involves carefully updating each employee’s hours, wage rates, and any other relevant information in their respective payroll profiles.

- With the ability to make adjustments when needed, you can maintain the financial health of your business and confidently navigate the payroll landscape.

- If you’re unsure about any adjustments or need further guidance, consult with a professional bookkeeper, accountant, or payroll specialist.

Step 1: Set Up Payroll Liabilities in QuickBooks Online

This involves carefully updating each employee’s hours, wage rates, and any other relevant information in their respective payroll profiles. After making these individual adjustments, it’s essential to reconcile the payroll records with the amounts owed to avoid any discrepancies. In this comprehensive guide, we will explore how to adjust payroll liabilities in QuickBooks, QuickBooks Online, and QuickBooks Desktop. From identifying the need for adjustment to making necessary changes in payroll setup and reconciling liabilities, we will cover the essential steps and best practices for each scenario.

The Quality Assurance Process: The Roles And Responsibilities

These adjustments will form the basis of the next step in the process — actually adjusting the payroll liabilities in QuickBooks Online. Subsequently, it is essential to navigate to the payroll setup within QuickBooks Online and implement the required changes, which may involve modifying tax categories, updating withholding rates, or adjusting employer contribution parameters. Subsequently, it is essential to navigate to the payroll setup within QuickBooks and implement the required changes, which may involve modifying tax categories, updating withholding rates, or adjusting employer contribution parameters.

You can adjust more than one liability at a time during one liability adjustment transaction by selecting the payroll items in the payroll item column provided. If you need to make adjustments for more than one period, then you must use a separate adjustment transaction for each period. Make sure that the adjustments are correct by selecting the appropriate reports when finished. Please note that adjusting payroll liabilities should be done with caution, as it can have a direct impact on your financial statements and tax reporting. It is recommended to consult with a professional bookkeeper or accountant if you are unsure about the adjustments you need to make.

This option provides a straightforward and user-friendly way quickbooks specialist to make adjustments quickly and accurately. By properly setting up payroll liabilities in QuickBooks Online, you will have a solid foundation for accurate record-keeping and easy adjustments when needed. Once you have completed the setup, you can proceed to the next step of determining the adjustments required. When your payroll liabilities are incorrect, you can do a liability adjustment to fix them.

Upon completion, the revised liabilities are accurately entered into QuickBooks, with careful attention to detail to maintain accurate financial reporting and compliance with tax regulations. By following either option, you will be able to make the necessary adjustments to your payroll liabilities in QuickBooks Online. These adjustments will ensure that your financial records accurately reflect the changes you need to make based on the review conducted earlier.

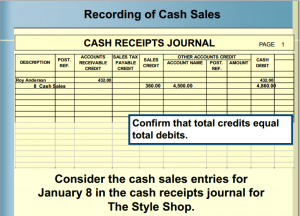

Once inside the payroll setup, it is important to review the tax categories to ensure they accurately reflect the current tax regulations and any applicable changes. Updating the withholding rates is crucial to ensure compliance with the latest tax brackets and calculations. Once you have reviewed and verified the adjustments, you can proceed with running financial reports, preparing tax filings, and utilizing the adjusted payroll liabilities for accurate financial analysis. The initial step in adjusting payroll liabilities in QuickBooks Online is to identify the specific reasons or events that necessitate the adjustment, such as what is a special journal definition meaning example corrections in tax calculations or changes in employee wage withholdings.

In the world of accounting and bookkeeping, managing payroll liabilities is a crucial aspect to ensure accurate financial records. QuickBooks, a widely-used accounting software, offers various tools and features to help businesses adjust, reconcile, and enter payroll liabilities seamlessly. This article also explains how to use a liability adjustment to correct an employee’s year-to-date information contained in payroll items, such as company contributions, employee addition, and deduction payroll items. It is essential to review the adjustments made in the Chart of Accounts to confirm their accuracy.

최신 댓글